Are You Behind on Your Student Loan?

An epidemic of student loan defaults is sweeping the country. Students, who previously were able to land solid jobs after college, now often find themselves forced to take lower-paying positions than they are qualified for while their higher-education credentials languish. Acutely pinched by the new economy, many thousands of graduates have been forced to move back in with their parents/siblings or share spaces with friends in overpopulated apartments.

“Benjamin Franklin” In this world nothing can be said to be certain, except death and taxes.

While the economy is definitely on an upswing, the economic recovery simply isn’t expanding fast enough to accommodate many of these graduates who were left behind during the recession. The truth is, it may be years before they are able to locate satisfactory employment.

In the meantime, their student loans continue to accumulate interest. Many students had simply overlooked the consequences of graduating with debts far exceeding their starting salaries. In fact, while attending school many were promised far better wages than what they found after graduation.

Nationally, the average cumulative debt for someone graduating with a Master’s Degree is currently about $28,400. In many cases, the students are unable to pay the debt down in a timely way. Many have gone bankrupt, some in an attempt to gain a foothold in today’s economy, and others simply to try and get out from under their loan debt.

Unfortunately, not even bankruptcy will always forgive the loans these students took to finish college. A whole new market space has sprung up with companies who specialize in “eliminating” or consolidating student debt.

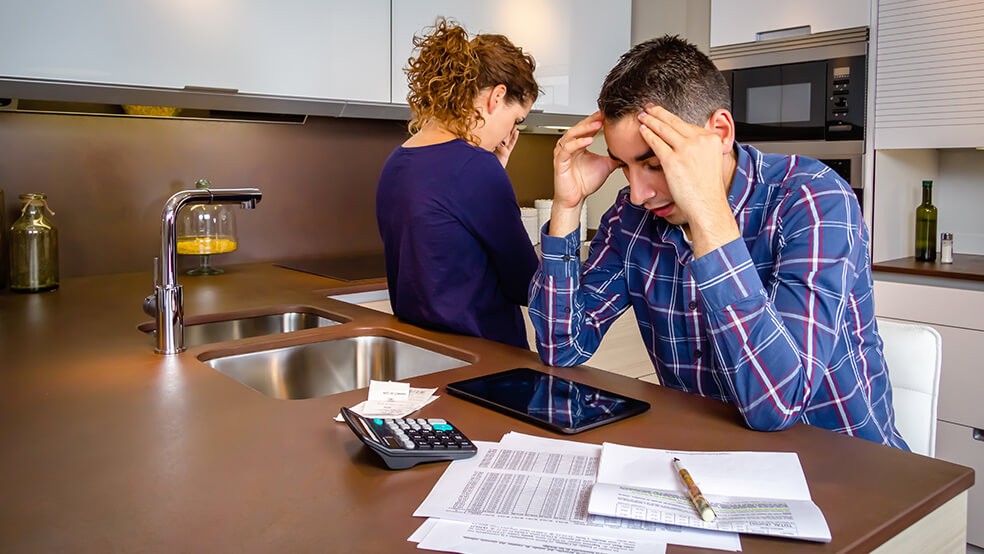

For George and Sarah, of Chatsworth CA, it was a combination of over-optimism, pride and plain bad luck. They met at UCLA and have been together for more than five years. They love each other, but admit their decision to get married two years ago was as much about necessity as it was love. They needed to save money on taxes and also to offset the high cost of maintaining two residences. Between the two of them they have over $40,000 in education debt.

They are both graduates, now. George graduated in 2011, with a Master’s in Civil Engineering and Sarah graduated in 2012, with a Master’s in Health Education. They struggled almost immediately with loan payments and then, even as Sarah prepared to return to UCLA to go after a PHD, she became pregnant unexpectedly. Their daughter Christina was born in 2013. Christina was diagnosed as autistic in 2014. The combination of lower salaries, high loan payments and the cost of fulltime daycare pushed them beyond their capabilities.

[blockquote author=”Sarah (Chatsworth CA)”]We had paid back all the interest on our loans. The principal debt on our private loans was about $1,000 beneath the original. Our federal loans were about $2,000 below the principle, but we had a ton of credit card debt and with Christina’s special needs, I had to keep working for the health insurance. I couldn’t go back to school.[/blockquote]

They spoke to a tax attorney, who basically told them there was no alternative to making the loan payments. “Even death won’t discharge some private loan debts.” He said.

Sarah’s father offered to pay off the debts, but George was too proud. The attorney also advised them to stick with the installments, as the loan repayment would positively impact their credit score. Loan providers, according to the lawyer, interpret lump-sum repayment as a “gift,” and do not report it to a credit score provider.

Two months later George was laid off at his workplace. It took him nine months to find even marginally suitable employment. By that time, they were both in default.

Federal law requires the student loan servicing agency to follow due diligence to collect payments even if a loan is delinquent, prior to declaring a loan in default. The agency makes repeated attempts to contact and inform borrowers of their delinquency and to collect late payments. If they fail at this, the agency can and will declare the loan as defaulted. They will also exercise the loan acceleration clause, making the full loan balance due and payable.

If you are in default on your federal student loans (behind by 270 days or more), the Department of Education can then take your tax refund using the Treasury Offset Program (TOP), which authorizes federal payments such as student loan tax refunds or Social Security income to be forfeited to pay debts owed other federal agencies. There are a few limited consumer protections, but debtors are usually unaware of them.

Any defaulted federal student loan can be “offset” by tax refund seizures. This “offset” process involves the full or partial seizure of the delinquent borrower’s federal tax refund. This is done sometimes without notice. It has become so common that the IRS has set up a hotline 800-304-3107 for individuals who have not received their refund and have reason to believe the refund has been seized. If your refund has been seized to offset a portion of your student loan, you have no recourse.

What about relief for student loan debt?

President Obama has asked the Treasury and Education departments and the Consumer Financial Protection Bureau to report back to him by October 1, on whether bankruptcy laws or other laws or regulations need to be be changed for student loans.

The William D. Ford Direct Loan program (Obama’s name was attached when the President reformed part of the Direct Loan program in 2009 under the Health Care and Education Reconciliation Act of 2010) offers alternatives for students taking loans to finish college. But, all benefits of the programs are offered only for federal student loans. Private loan borrowers do not qualify.

The gist of the reforms include:

- The federal government will no longer subsidize private lending institutions for federally backed loans.

- Starting in 2014, new loan borrowers will qualify to make payments based on 10% of discretionary income.

- Starting in 2014, new loan borrowers will be eligible for loan forgiveness after 20 years instead of 25 (on qualifying payments).

- Federal money will be used to fund poor and minority students and increase college funding.

There are several different repayment plans, most notably the Income Based (IBR) This plan bases the borrower’s payment strictly on income and family size. The balance of the loan and interest rate are not used in calculating a monthly payment. The borrower would be responsible to pay 15% of their discretionary income to their federal student loans. Borrowers in the IBR can have a payment as low as $0.00/mo. For example:

A borrower owes $40,000 at an interest rate of 6.875 percent, with a 25 year term. If the borrower is single with an adjusted gross income of $25,000/yr. The interest on this loan would normally be $229.17 per month, but the borrower would qualify for an IBR payment of $93.69. The borrower would be forgiven $135.48 of interest per month. If the borrower’s financial situation does not change for three years, they would be forgiven $4,877.28.

This of course, does not help George and Sarah. They are seeking to find a way out of their debt quagmire using the Public Service Loan Forgiveness program, designed to reward people who opt to work lower paying jobs in the public sector, or work for non-profits. If they qualify, they will be required to make 120 income based payments, and the balance remaining on your after the 120 payments would be forgiven.

If George and Sarah qualify for Public Service Loan Forgiveness program, they will still be paying on their loans for 10 years. They will both be 40 before their loan has been satisfied. Their only hope is that the government comes up with better legislations concerning student loan debt, and this could happen. The student loan issue has become a hot button topic and more legislation is being drafted as this is written. In fact, a proposal to allow students who work to receive a free first two years of junior college has been proposed.

What can you do if your refund was seized?

People who have student loans in default should get a notice in advance, a warning they are at risk of having a tax refund seized for student loan repayment. The notice contains instructions for a review of your loan information and how to avoid the offset.

If your tax refund is seized, you can still request a hearing. If it was taken by error, the money will be refunded. However, be aware that an error does not generally include not getting a notice; it typically would require that you be able to prove your student loan was not in default.

The best hedge is to adjust your withholdings whether you’re subject to a student loan tax refund offset or not. If you generally get a large tax refund means you’re probably overpaying your taxes during the year and economically that’s a bad practice. If you are in default on your federal student loans you probably could use the excess money you are having withheld. You can’t change your withholding from last year, but you should reconsider how much you’re having withheld for taxes to give you both more money during the tax year and less liability should you default.

The bigger problem is how to deal with the default on your student loans from going forwward. You’ll want to quickly get out of default and remain solvent. There are payment options and you should be able to make one work for you. For some, income-based payments can be set as low as $0. And if your situation is dire and expected to remain so, bankruptcy and the discharge of student loans might be the only option.

The only case in which you are likely to be to recover the money is if you filed jointly with a spouse, and it was his or her student loan that was in default. You might qualify for an injured spouse claim.

But, for most, the past is past. The best thing you can do is think things through and understand your options. If you haven’t filed your tax return but expect a large refund, it’s imperative you have a clear idea of what options you have to get out of default before filing.

A student loan default can squeeze your budget and it can ruin your credit, costing you thousands of dollars in higher debt costs and percentage rates over your lifetime.

What about George and Sarah? Well, they did qualify for the Public Service Loan Forgiveness program and they are on their way to paying off their student loan debt. As George says, “Only 115 payments left.”

My Tax Help MD provides the best IRS tax help and tax settlement services and make the life of its clients easy and relaxed. Having a team of professional tax consultants, we provide diverse IRS tax debt resolution service. You can tell us your tax problems and we will come up with the best possible solutions for them.

Call us at 888-557-4020 or contact us online at https://www.taxhelpmd.com/contact-us/